What Inflation Really Means for Canadians — and How to Plan for It

Inflation affects nearly every aspect of our financial lives — from the price we pay at the grocery store to the cost of borrowing for a home. Even when official inflation numbers seem modest, many Canadians still feel the pinch in their daily budgets.

So why is there often a disconnect between what the numbers say and what we experience? And more importantly, how should we respond as individuals and households?

Whether you’re a homeowner, a renter, a saver, or an investor, understanding inflation is key to making better financial decisions. Let’s dive in.

What is meant by Inflation

Inflation is the rate at which the overall price level of goods and services rises over time, leading to a decrease in the purchasing power of money. In simple terms, when inflation goes up, your dollar doesn’t stretch as far — you pay more for the same items.

In Canada, the most common way to measure inflation is through the Consumer Price Index (CPI). The CPI tracks the average change in prices over time for a fixed “basket” of goods and services that a typical household might buy — including essentials like groceries, rent, gas, clothing, and more.

Each item in the basket is weighted based on how much Canadians, on average, spend in that category. For example, housing usually has a larger weight than entertainment because it takes up a bigger portion of household budgets.

Inflation data is collected and published by Statistics Canada, which updates the CPI monthly. The Bank of Canada (BoC) monitors this data closely and uses it to help guide its monetary policy decisions — especially interest rates. The BoC’s target is to keep inflation around 2%, which is considered stable and healthy for economic growth.

By understanding how inflation is measured and reported, Canadians can better interpret economic headlines and make informed financial choices.

Inflation/CPI Basket

The CPI basket is a collection of nearly 700 goods and services that represent the average household’s spending. These items are grouped into major categories such as:

- Housing

- Food

- Transportation

- Clothing and footwear

- Health and personal care

- Recreation and education

- Alcohol, tobacco, and cannabis

- Household operations

But not all items are weighted equally. Each category is assigned a weight based on how much the average Canadian household spends on it. For example, if housing represents about 30% of the average household’s expenses, then changes in housing prices will carry more influence on the overall CPI than smaller spending categories like clothing or recreation.

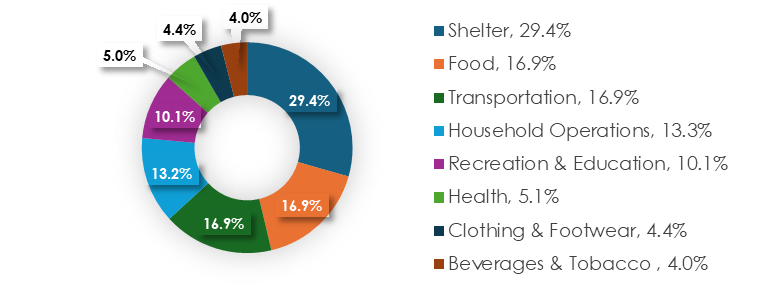

Current CPI Basket

Statistics Canada updates the CPI basket weights every two years, using detailed household spending data from surveys like the Household Final Consumption Expenditure (HFCE). This helps ensure the index reflects how Canadians actually spend their money.

For example, if more households are spending on streaming services instead of cable, or shifting from buying new vehicles to using rideshares or public transit, the basket is adjusted accordingly.

The CPI basket covers eight major spending categories. Each category is assigned a weight that reflects how much of the average household’s spending goes toward it. Here’s how the 2024 basket looks:

Current Inflation/CPI Basket as on May 2025

Statistics Canada reviews and updates these weights every two years, using national household spending data. The 2024 update reflects changes in how Canadians spend—such as an increase in services within categories like household operations (now 58.17%) and recreation (now 59.25%).

These updates ensure the CPI remains relevant and representative of real-world spending patterns.

Types of Inflation the Bank of Canada Watches

While most headlines focus on the headline CPI, the Bank of Canada (BoC) looks much deeper when deciding how to steer the economy. That’s because not all price changes are created equal — and some are more persistent than others.

Headline CPI: The Broadest Measure

Headline CPI is the year-over-year percentage change in the overall Consumer Price Index. It reflects the average price movement across all items in the CPI basket — including food, gas, rent, clothing, and more.

This is the number you typically see in the news. But it can be volatile, often influenced by seasonal factors or external shocks (e.g. energy prices, food supply issues).

Core Inflation: A Clearer Signal

To get a clearer view of underlying price trends, the BoC tracks three core inflation measures:

| Core Measure | What It Does |

|---|---|

| CPI-common | Tracks price changes that are common across many categories — a broad signal of underlying inflation pressures. |

| CPI-median | Measures the price change at the midpoint of all components — eliminates extreme highs and lows. |

| CPI-trim | Removes the top and bottom 20% of price movements — filters out the most volatile items. |

Together, these help the BoC understand how widespread inflation is — and whether it’s being driven by a few outlier categories or is more systemic.

Why the BoC Uses Multiple Measures

Inflation is influenced by many moving parts — global commodity prices, domestic wage growth, supply chain disruptions, and more. No single number can fully capture the complexity. That’s why the Bank of Canada relies on a set of core measures rather than just the headline CPI. By examining CPI-common, CPI-median, and CPI-trim together, the Bank can better assess whether inflation is broad-based or driven by a few volatile categories. This multi-measure approach helps the BoC avoid overreacting to temporary price spikes (like fuel or produce) and instead focus on longer-term, underlying inflation trends that matter most for monetary policy.

How This Influences Interest Rate Policy

The Bank of Canada’s primary goal is to keep inflation close to its 2% target over time. To do this, it adjusts its key policy interest rate based on the signals it receives from these inflation measures. When core inflation consistently runs above target, the Bank may raise interest rates to cool down consumer demand and reduce inflationary pressure. On the other hand, if inflation is below target or the economy shows signs of slowing, the Bank may lower rates to encourage borrowing and spending. These rate changes directly affect mortgage costs, savings account returns, and the broader economy — which is why understanding how inflation is interpreted by the BoC is essential for making informed financial decisions.

Why Supermarket Prices Feel Different

Many Canadians feel like their grocery bills are rising faster than the inflation rate — and in many cases, they’re right.

Food prices are more volatile than other items in the CPI basket. Factors like weather disruptions, supply chain issues, fuel costs, and global commodity prices can cause sharp swings in food costs.

While the headline CPI includes food and energy, the core inflation measures used by the Bank of Canada often exclude these volatile components to better reflect underlying trends.

This disconnect creates a psychological impact — households tend to notice frequent or sharp increases in essentials like groceries, even if other categories (like clothing or electronics) remain flat or fall in price.

In short, your personal experience with inflation may feel worse than the official number — especially if a big part of your spending goes toward necessities.

Six Planning Moves to Stay Ahead

1. Re-baseline your budget

Inflation creeps in fastest through everyday costs—groceries, fuel, utilities—so refresh those line items with current prices at least twice a year. Trim or pause non-essentials (streaming, dining out, subscriptions) first; you’ll preserve cash flow without sacrificing necessities.

2. Boost the emergency fund

The old three-month cushion is thin in a higher-cost world. Aim for four to six months of essential expenses so unexpected price spikes or job gaps don’t force high-interest borrowing. Keep this money liquid—in a high-interest savings account or cashable GIC.

3. Review debts & mortgages

If your mortgage or HELOC renews within 12 months and you expect rates to rise, explore locking in a fixed term now. For HELOCs and other variable-rate debt, accelerate payments—especially where interest isn’t tax-deductible—to reduce exposure to future rate hikes.

4. Stay invested, stay diversified

Long-term growth still comes from equities, but inflation hedges add stability. Consider Canadian Real Return Bonds, global infrastructure or REIT ETFs, and a mix of domestic and international stocks. Resist the urge to sit in cash—after-inflation returns there are usually negative.

5. Inflation-proof retirement projections

Model future expenses with at least 2 % annual inflation. To protect purchasing power, look at annuities that index with CPI or delay CPP/OAS; each year of deferral raises your guaranteed, inflation-linked benefit for life.

6. Use tax-sheltered buckets wisely

Max out your TFSA first—tax-free compounding outpaces taxable interest, especially when inflation pushes nominal returns higher. RRSPs remain valuable, but remember rising CPI also nudges tax brackets and credits upward, slightly dampening future tax drag. Keeping new savings in these shelters helps your real (after-tax, after-inflation) returns stay ahead of rising prices.

Closing Remarks

Inflation isn’t just a single number — it’s a measure of how the overall cost of living changes over time. While the CPI gives us a national average, individual experiences can vary widely, especially with essentials like food and housing often rising faster than the headline rate.

By understanding how inflation is measured and how it influences interest rates, Canadians can make smarter financial choices, from budgeting to managing debt and investing. Staying informed and proactive is the best way to keep your finances resilient in an inflationary world.